Apple Business isn’t competing with telecom operators, it’s redefining what they’re needed for

Shifting Control Layer in SMB IT... Implications for Android, Verizon, AT&T, T-Mobile, and the Future Role of Telecom Operators

Apple Business Is a Control Shift

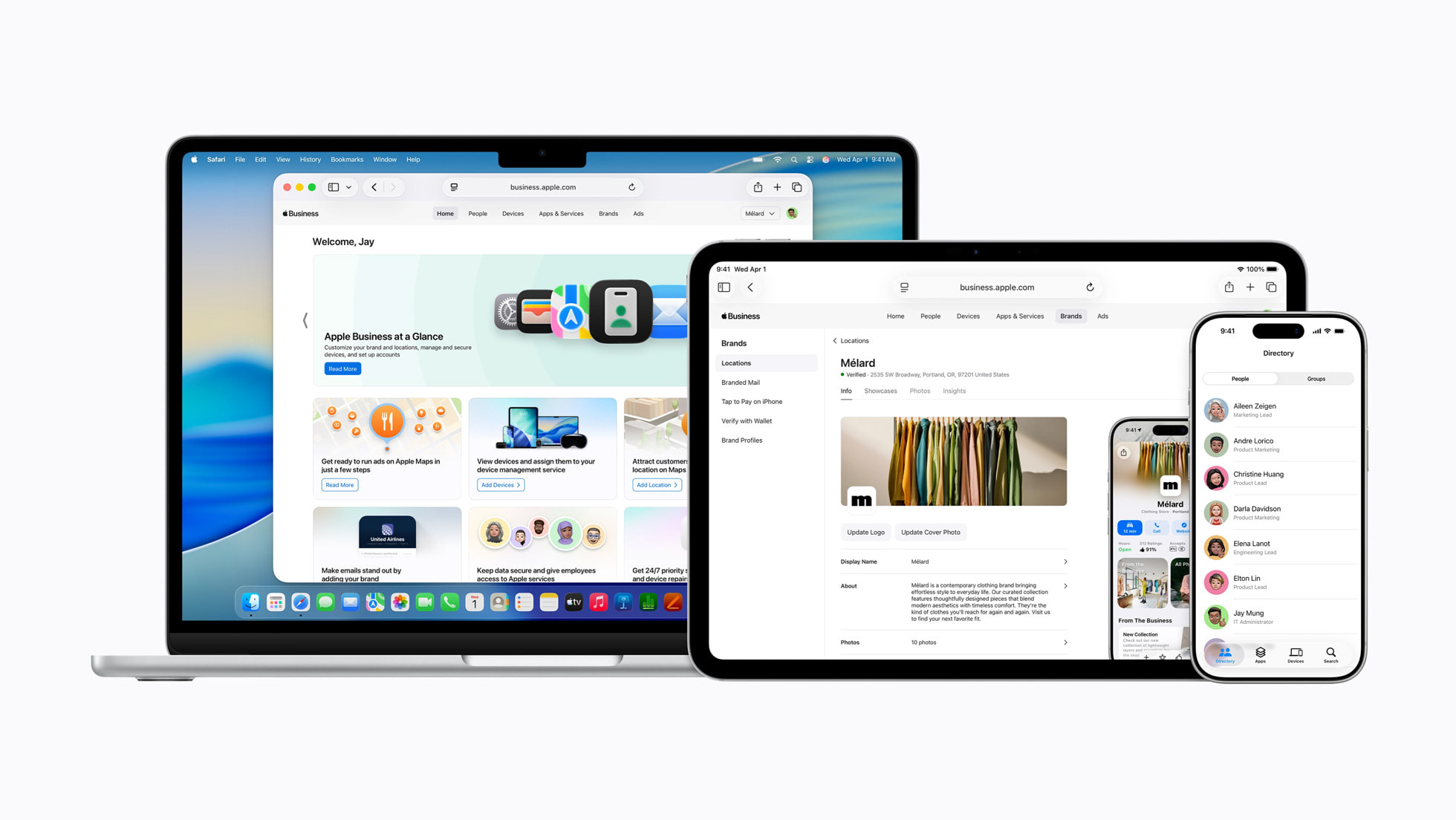

Apple’s introduction of Apple Business will likely be interpreted by many as a packaging exercise, a logical consolidation of existing capabilities such as mobile device management, email, and identity into a single platform.

Apple Business announcement - 03/2026

That interpretation understates what is actually happening.

Apple is not simply bundling tools. It is repositioning itself as the default operating layer for small and mid-sized business IT.

For years, the SMB technology stack has been fragmented. Businesses relied on a mix of telecom operators, managed service providers, and SaaS vendors to assemble a functional environment: connectivity from a carrier, email from Google or Microsoft, device management from a third-party provider, and various tools layered on top. Operators, in particular, attempted to capture more value by bundling mobility, unified communications, device management, and basic security into integrated offerings.

Apple Business collapses much of this complexity. It embeds core IT functions directly into the device ecosystem and presents them through a unified, simplified interface. For SMBs without dedicated IT resources, this reduction in friction is not incremental.

The strategic implication is clear. The center of gravity for SMB technology decisions is shifting away from multi-vendor integration and toward platform selection. Choosing a device ecosystem increasingly determines the rest of the stack.

This has immediate consequences across the industry. It raises the bar for Android’s enterprise positioning, places pressure on operator-led mobility and MDM monetization strategies, and introduces Apple into adjacent domains such as local business discovery through Maps advertising.

More fundamentally, it reframes the role of telecom operators. The question is no longer how operators can expand their service footprint on top of connectivity. It is whether they can maintain relevance when the primary control layer sits above the network.

A Structural Shift in the SMB Value Stack

The SMB market has historically rewarded vendors that could simplify complexity. However, simplification typically requires coordination across multiple providers, creating opportunities for operators and MSPs to act as integrators.

Apple Business changes that dynamic by removing the need for integration in the first place.

Core capabilities such as device provisioning, identity management, application distribution, and basic productivity are now:

Pre-integrated

Native to the operating system

Available at low or no cost

As a result, several long-standing monetization layers are being compressed simultaneously. Services that once justified recurring fees are becoming baseline expectations.

At the same time, Apple is extending its reach into customer acquisition through Maps-based advertising, creating a direct connection between business identity, discovery, and transaction within its ecosystem.

Taken together, these moves indicate a broader shift: value in the SMB segment is moving away from connectivity and adjacent services and toward platform ownership and ecosystem control.

What This Means Immediately

In the near term, three conclusions stand out.

First, Apple is redefining the baseline for SMB IT. What previously required multiple vendors and a degree of technical coordination is now accessible through a single platform experience.

Second, the traditional “attach” model — where operators and partners layer additional services on top of connectivity — faces structural pressure. When core capabilities are embedded and free, differentiation becomes significantly more difficult.

Third, the locus of value is shifting upward. Control over identity, device management, and application distribution increasingly determines the customer relationship, while connectivity risks becoming a supporting layer rather than the primary interface.

The remainder of this report examines the implications in detail, including the impact on Android and Google’s ecosystem, the specific exposure of operators such as Verizon, and the strategic options available to telecom providers over the next three to five years.